Wednesday, September 29, 2010

Message to the Fed: this is the modern monetary theory (MMT) transmission mechanism.

It seems a number of Fed and ex-Fed people have at last tumbled to the fact that there are serious problems with traditional ideas on money supply transmission mechanisms.

This Fed paper to which Warren Mosler draws attention points to the fact that there has been a 2,173% rise in bank reserves in the last two years, with (contrary to text book predictions) almost no effect. Yes you read that right: 2,173%.

The authors of the Fed paper also say “if the quantity of reserves is relevant for the transmission of monetary policy, a different mechanism must be found.”

And then there is Arnold Kling, who worked for a time as an economist for the Fed. He says “I am having an equally hard time understanding modern monetary theory.”

In view of the above, it might be helpful to set out the MMT transmission mechanism. It is very simple and it’s thus (as I see it).

1. The government-central bank machine net spends in a recession. Assuming government wants the relative sizes of public and private sectors to remain constant, some of the money will be spent on hiring extra public sector workers and/or making sure that tax shortfalls don’t result in public sector workers being sacked. That creates employment.

2. There is a multiplier effect from “1”, that is, part of the above additional payroll costs will be spent, which in turn employs more people.

3. The above additional public sector workers will probably save some of their income. That boosts private sector savings. Those savings will not expand for ever. The point will come where the private sector thinks it has enough by way of savings, at which point it will cease saving and will spend, or try to spend all its income. That employs yet more people.

4. While the above boost for the public sector boosts the private sector INDIRECTLY, it is probably desirable to give the private sector a DIRECT boost as well. That can be done by, for example, reducing payroll taxes or income tax. That boosts employees’ take home pay, which in turn will boost their spending, which employs more people.

Doubtless some of the above private sector increase in take home pay, will be saved. The consequences are exactly the same as with the above public sector employees. That is, savings will rise to the point where no more savings are required, etc, etc.

Sunday, September 26, 2010

Von Mises and whether U.S. unemployment is structural.

One of the main claims made ad nausiam by the Von Mises brigade is that recessions are needed so as to rid the economy of what they call “malinvestments”.

The first flaw in this idea is that in any medium size or largish economy, even in periods of full employment, thousands of firms go bust per week and thousands of new firms start up per week. That is, there is a continuous process of disposing of “malinvestments”. Thus the mere existence of malinvestments does not justify recessions.

Second, every economy is stuffed full of malinvestments in that about 25% of industrial capacity is normally unused.

Third, it is a bit of a mystery as to why the existence of thousands of empty houses going to rack and ruin should stop a country’s workforce being employed in non construction type activities. Moreover, the construction industry has not DISAPPEARED as a result of excess house building: it just halved in size, or thereabouts.

Fourth, if excess demand results from easy credit, this will result in excess investment in a WIDE RANGE of industries, plus it will result in inflation. Now inflation in the U.S. was a percentage point or two above target just before the credit crunch: a negligible problem. In contrast, the REAL problem was the grotesque inflation in house prices and ludicrous mortgages being offered, like the famous NINJA mortgages.

This leads to a more plausible argument which might be the basis for thinking that the economy cannot bounce straight back to where it was pre-crunch. This is that a large excess supply of former construction employees amongst the ranks of the unemployed might mean that it will take time to retrain those people, hence hindering a return to full employment as quickly as we would like. So does the evidence for this phenomenon stack up? The answer is “possibly, but it’s a bit doubtful”.

First, if the latter were a significant problem, one would expect to find significantly more former construction employees amongst the unemployed (relative the size of the construction industry) than former members of other industries. This does not seem to be the case if this Roosevelt Institute study is anything to go by: see charts on page 8 here.

In contrast to the above study, and study done by “Oregon Business Report”, paints a slightly more gloomy picture. On the other hand, according to this study, the expansion in numbers employed in the Oregon construction sector between 2001 and 2009 was identical to the contraction 2007 – 9. Now if the workforce are flexible enough to move INTO construction from a variety of other sectors of the economy, presumably they are flexible enough to move back again (though admittedly the contraction was faster than the expansion).

In contrast to the Oregon study Also this study claims that construction workers have no more difficulty finding alternative work than the national average. Since the latter study covers the naton as a whole rather than just one state, it is presumaly more reliable.

As to strictly theoretical considerations. Suppose the level of unemployment at which inflation becomes excessive is 4%. Suppose the proportion of the workforce employed in construction at its height two years ago was 6%. Suppose numbers employed in construction halve, and that of those becoming unemployed, a half have serious difficulty finding other jobs without retraining. That means the proportion of the workforce who are seriously difficult to place is (6/2)/2 which is 1.5%. That in turn means the overall level of employment at which inflation becomes a problem rises from 4% to (4 + 1.5) = 5.5%.

That is an insignificant rise compared to the actual rise over the last two years. Conclusion: there isn't a huge "structural" problem.

Friday, September 24, 2010

Peter Peterson: economic genius.

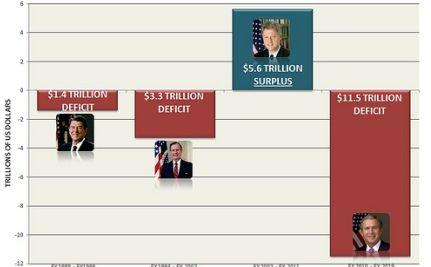

Peter Peterson is a billionaire who spends a significant proportion of his wealth every year promoting the idea that the deficit and national debt must at all costs be reduced. So does he have any particularly bright ideas to back this claim?

The answer is “no”. The ideas put by the Peterson Foundation site are about as simple minded as it is possible to be. The ideas are set out in an article entitled “A Path to Balance”. (There is a link to the article from the Foundation’s site – see the “This paper” link in orange.)

This article is easily comprehensible to a ten year old: that’s how sophisticated it is.

The article starts with two charts, the first of which shows the deficit as a proportion of GDP rising from about zero in 1949 to an average of (shock horror) about 4% for 2001 to 2009. That of course is grossly misleading because in 1949 national debt was at a near record level as a result of WWII and was rapidly being paid back. You’d expect no deficit in those circumstances: indeed you’d expect the occasional surplus. Collecting tax and using the money to pay back the national debt is almost the definition of “surplus”.

Just under that chart is another, showing national debt as a proportion of GDP declining from around 80% in 1949 to roughly 40% in the seventies and eighties, and then rising again to roughly 60% in 2010. What this omits, because it would spoil the Peterson story, is that the debt was over 200% just after WWII. That is, Peterson wants us to think that a rise to much more than the 80% level is some kind of disaster. That’s a bit hard to reconcile with the fact that the debt was well over 200% just after WWII. So we just keep quiet about that, don’t we?

The Peterson master plan is to gradually reduce the debt: a stroke of genius! That sounds much like a household gradually paying off its mortgage. The latter, of course, is microeconomics: about as relevant to paying off a national debt as chalk is relevant to cheese, because national debts, deficits and so on are macroeconomics, whereas individual household mortgages are microeconomics.

The first big problem with gradually paying off national debt at some pre-determined rate over the next ten years or so is that it might be a totally inappropriate policy in say five years time. For example, if there was an outbreak of irrational exuberance and general all round confidence in five years time, with the economy booming and excess inflation just round the corner, then some form of deflationary policy would be needed: for example raising taxes and paying off the national debt much faster than under the above “ten year plan”!

The second big problem is that collecting extra tax (and/or reducing public spending) is deflationary. Thus the basic effect of the “ten year pay back” scheme is deflationary. That could be wholly in appropriate if the economy stays in the doldrums over that period. So what to do?

Well there is an amazingly simple solution. Indeed, this solution could, at least in theory, wipe out the debt in just one year. Here’s how.

First print money and buy the debt back. That on its own would doubtless be too stimulatory and inflationary. Solution: mix the latter policy with a deflationary method of paying the debt back, that is raise taxes (or reduce government spending) and use the money collected/saved to buy the debt back.

Mix the above deflationary and stimulatory/inflationary measures in the right proportion, and you have a neutral pay back arrangement: no excessive inflation or unemployment while paying back. Indeed, the elements of the above solution can be altered to produce any desired outcome. For example for a more stimulatory stance while effecting the pay back, implement a bit more money printing and a bit less tax increase / public spending reduction.

There is just one problem (and one only) with the latter “wipe the national out” system: it would probably involve too much dislocation if started and completed on just one year. That is, it would be difficult to effect without some abrupt changes in the tax paid by particular groups, and that would bring political problems.

But, essentially paying the entire national debt back in a few years, at the same time as adopting any amount of stimulus or deflation you like is not difficult: how to do it can be explained to an intelligent ten year old. For more on this, see here.

Thursday, September 23, 2010

Robert Reich is near to advocating Modern Monetary Theory.

Robert Reich says, quite rightly, that interest rates cannot be dropped any further.

He then points out, correctly, that “The problem is consumers, who are 70 percent of the economy. They can’t and won’t buy enough to turn the economy around.” Agreed.

Put that another way, THE FUNDAMENTAL PURPOSE OF AN ECONOMY is to produce what the consumer wants. In view of this, it might have been an idea, right at the start of the recession, to have given the consumer more of that amazing stuff which ENABLES consumers to go out of buy what they want. And that amazing stuff is called MONEY!!!!!! That would have been better than ar*sing around with interest rates, QE, stuffing the pockets of Wall Street crooks and fraudsters, etc, etc.

Incidentally, in addition to waving their credit cards in the air and demanding various products, consumers also demand (via the ballot box) various publically provided goods and services. So the provision of these also needs to be expanded (or at least not allowed to fall) in a recession – as advocated by Modern Monetary Theory (MMT).

Reich continues: “So what’s the answer? Reorganizing the economy to make sure the vast middle class has a larger share of its benefits. Remaking the basic bargain linking pay to per-capita productivity.” Certainly the middle class (in addition to the lower orders, perhaps) needs more spending power. But there does not need to be a close link between pay and productivity in an MMT scenario.

In particular, come a recession, it would be a good idea to feed more of the above mentioned “amazing stuff” into employees pockets: that is, it is desirable to have employees pay move ahead of productivity, at least for a while. Conversely, given an outburst of irrational exuberance, it would be desirable to have pay fall behind productivity.

Robert Reich: please keep thinking. You’re almost there.

Wednesday, September 22, 2010

Monday, September 20, 2010

Governments taylor their economic policies to account for the economic illiteracy of their populations.

Britain’s finance minister, Alistair Darling, created £60bn out of thin air for the benefit of two banks, RBS and HBOS, when they were in trouble, but didn’t announce what he had done till about eighteen months later. Why? I think it was for much the same reason as Keynes backed a policy he knew quite well was second best.

Keynes said that in a recession governments should borrow and spend. Abba Lerner said governments should just print money and spend it. Keyes was well aware of the “print” option, but seems to have favoured the borrow option because it looked or sounded more respectable or sensible.

Keynes said of Lerner, “"Lerner's argument is impeccable but heaven help anyone who tries to put it across to the plain man at this stage of the evolution of our ideas.”

There is something unhealthy about governments pursuing policies they know to be flawed or second best, simply to take account of the economic illiteracy of the population or the “common man”.

To avoid the above problems in future, the ideal would be to make economics a compulsory school subject, with particular emphasis on when money printing is inflationary and when it is not. But not much chance of that, I suppose.

Thursday, September 16, 2010

I love the ignorance of the anti-stimulus lobby.

“The free market will sort it out….no need for stimulus.” That’s the message of a hundred anti-stimulus articles.

The monster and glaring omission from nearly all these articles is any explanation as to exactly HOW the market gets out of a recession. The latter question was much debated in the 1930s. But, hey you don’t think the anti-stimulus red-necks have actually studied these debates do you?

There ARE actually two mechanisms via which the free market recovers from recessions: the Pigou effect and Say’s law. But Keynes concluded, quite rightly I think, that while these effects work in the long run “in the long run we are all dead”. I.e. these effects do work, but they work too slowly.

But don’t bother trying to find out what the anti-stimulus lobby think about Say or Pigou: most of them haven’t even heard of the two latter indivduals.

Examples of anti-stimulus articles:

1. by Greenspan (of all people):

2. This article is by Garett Jones, a Prof. at George Mason University. In addition to apparently never having heard of Say or Pigou, he seems to think that micro-economic laws work at the macroeconomic level: that is, he thinks that an all round wage cut reduces unemployment. Does he even know there is a distinction between macro and micro?

Tuesday, September 14, 2010

Modern Monetary Theory.

One of the beauties of Modern Monetary Theory (or indeed any half intelligent macroeconomic regime) is that under such a regime a whole series of pseudo problems and non problems raised by economic illiterates come out in the wash. That is, these non problems, which so called economists spend months trying to sort out, solve themselves.

First example: Tim Congdon worries about the possibility that tighter bank regulation will thwart the recovery. To be more exact, Congdon (like many leading conventional economists) has long been hooked on monetary aggregates, with little appreciation of the difference between who holds any additional money (e.g. Main Street or Wall Street). Certainly those in charge of sorting out the crunch put the bulk of recovery money (bar the automatic stabilisers) into Wall Street rather than Main Street.

Tighter bank regulation probably IS deflationary. But what of it? If tighter regulation is needed to reduce the chances of another crunch, then so be it. The deflationary effect can always be countered by extra stimulus.

And given that interest rates are currently as low as they can go, the only remaining option is expanding government spending (as prescribed by MMT) or tax cuts (as prescribed by MMT). And if any readers think that the two latter necessarily increase the national debt, please read Milton Friedman.

And as to the idea that we let banks indulge in undesirable practices because the effect is reflationary, you can bet your bottom dollar that clamping down more effectively on bank note forgery has a deflationary effect. Which proves that we should allow bank note forgery?

In short, we should pass whatever laws are deemed necessary in relation to banks, loan sharks and forgers. Whether the effect is deflationary or reflationary does not matter under an MMT regime. Reason is that under MMT, government just net spends to the point where the optimum relationship between inflation and unemployment is attained. If tighter bank regulation IS deflationary, the Treasury and central bank will react automatically under MMT by increasing net government spending.

In other words Congdon does not get the point correctly made by Winterspeak*, namely that the deflationary effects of tighter bank regulation can perfectly well be nullified (and more than nullified) by stimulatory measures. The result would be less bank based economic activity and more non-bank based economic activity. In view of the disastrous effects of banks over the last few years, less bank based activity would on the face of it be highly desirable.

*See Winterspeak’s 17th Sept 2010 post “The Fatal Flaw is Economists.”

Second example of a non problem comes from an Economist article.

This article points to the fact that the corporate sector is hoarding cash, and makes the bizarre claim (in the sub heading) that “For the recovery to proceed smoothly, firms must stop hoarding cash.”

So does The Economist seriously claim that the corporate sector will respond to exhortations from The Economist? Unlikely.

A better solution to this vexed non-problem is to have government net spend till the optimum inflation unemployment relationship is attained. The corporate sector can save cash or dissave to it’s heart’s content – as long as government adopts the above net spending policy, what the corporate sector does won’t make much difference. It’s a problem that solves itself.

Monday, September 13, 2010

The new Basle rules would not hamper economies even if we ignore the beneficial effects of reducing the chance of another credit crunch.

The most popular and naïve assumption (an assumption which is even made in the Basel III reports) is that higher lending costs hamper economies. Though the Basle reports claim the benefits from a reduced chance of another credit crunch will override the “hamper” effect.

The idea that those tighter requirements represent a cost is based on the assumption that any old increase in lending is good, because, er, any old investment is good.

Well, there is actually an OPTIMUM amount of investment.

Now is the amount of investment currently optimum? No, it’s not. It’s actually more than optimum because maturity transformation lets borrowers borrow at lower rates than they otherwise would. And more stringent capital requirements effectively reduces the extent of maturity transformation. For more on this see here, (point No 1 in particular).

Friday, September 10, 2010

The similalrity between bankers and prostitutes.

Stamp out prostitution on one neighbourhood and the problem just shifts to another neighbourhood.

Supress unacceptable banking practices in one country, and banks just shift to another country.

That does not make bankers look good. So you might think that when bankers are asked why they object to some of some of their activities being curtailed, they’d come up with a better response than the above “prostitutes’” response.

But in an article in the Financial Times (Sept 9), the main response of three bankers was the above prostitute response. Don’t they realise they are shooting themselves in the foot?

BTW, those three “banker responses” seem to be in the paper edition of the FT, but not in the online version.

The best quote from this article comes from Sir Martin Taylor, Banking Commission member: “The investment banking activities of a universal bank were at all times parasitic on the retail bank balance sheet.” Quite right.

______________

Good idea in the letters page (same FT edition) from Nigel Reed, as follows. Bank splitting should be voluntary and the U.K. government should guarantee only deposits in the retail section of split banks. Result: unsplit banks can go to another country if they wish, but that country is accepting potentially toxic stuff.

Wednesday, September 8, 2010

Oh ma God: Stefan Karlsson thinks an all-round wage cut would raise employment.

Stephan Karlsson’s article is here. The article is reproduced below. My comments are in red.

__________

A basic truth of economics is that whenever supply exceeds demand, a lower price will reduce that excess and increase the number of actual transactions. On this issue, no disagreement exists between Austrians and neoclassicals.

Yet a surprising number of leading leftist economists deny this fundamental truth in the case of the labor market.

The question as to whether an all-round wage cut raises employment is a purely technical question. It has nothing to do with the political left versus political right argument. Dragging the “left versus right” thing into the argument is a distraction.

Debating this issue with Tyler Cowen and Bryan Caplan, particularly Paul Krugman and Rajiv Sethi tries to deny this. Needless to say, I agree with the Cowen-Caplan view and not the Krugman-Sethi. That a lower price will increase demand is so self-evident at least under normal circumstances that I won't bother to elaborate upon it. So I will instead directly adress Krugman's and Sethi's argument for why it does not apply under the current circumstances. I'll start with Krugman. Here are his first argument:

The all round wage cut question has nothing to do with “current circumstances”. For example heated debate took place on this topic in the 1930s

"Here’s how the fallacy works: if some subset of the work force accepts lower wages, it can gain jobs. If workers in the widget industry take a pay cut, this will lead to lower prices of widgets relative to other things, so people will buy more widgets, hence more employment.

But if everyone takes a pay cut, that logic no longer applies. The only way a general cut in wages can increase employment is if it leads people to buy more across the board. And why should it do that?"

First of all, there is no need to assume that all wages will be cut. Some sectors suffer from higher unemployment than others so wages will likely be lowered there more than others, causing a relative shift of employment from sectors with a relative shortage of labor to those with a relatively high unemployment rate.

The above para may well be correct, but this isn’t the central question being addressed here, namely the “all round wage cut” question.

Secondly, even if all wages were cut by an equal amount there are good reasons to assume it would increase the demand for labor (at least given the currently high level of unemployment). The reason for that is that while wage cuts would create a negative income effect for workers who would have been employed anyway, it would create a positive income effect for their employers (the capitalists) Assuming employment won't be affected, wage bargaining is a zero sum game between employers and employees.

And since income in other countries won't be affected, lower wages would through the substitution effect increase demand for American labor by foreigners (or in other words increase net exports). And that same substitution effect would increase demand for products made by American workers by American capitalists.

Yes, and by the same token there would be an exactly equal DROP in demand for goods coming from WORKERS for stuff made by American “workers and capitalists”. Ergo: no effect on employment in the aggregate.

Also if wage bargaining is a “zero sum game”, as Stefan assumes, (i.e. if every dollar of income lost by employees is a dollar of income gained by employers) then there is no effect on the price of goods!!!! Thus Stefan’s claim that demand for U.S. goods from abroad will increase is invalid.

And given the above factors, there are good reasons that aggregate income would rise as the losses of workers who would have been employed anyway is more than compensated by the gains of the capitalists and the workers who are employed because of the substitution effect.

Contrary to Krugman there is thus no need to assume that real interest rates would be lowered to realize that lower wages would increase employment.

As for Krugman's bisarre arguments in later posts that nominal wage cuts can't cut the real wage, it overlooks of course that the cost of products consists of more than just labor costs, and that demand for products doesn't just come from domestic workers, but also capitalists and foreigners.

There is nothing “bizarre” about Krugman’s arguments. If the wage of employees and employers were halved (or quadrupled, or multiplied by a million) tomorrow, there would be precisely and exactly NO effect on real incomes (if we ignore the administrative and bureaucratic costs of changing the price of everything by a factor of two, four, a million, or whatever you like). In the long run the REAL wages and incomes enjoyed by a particular country are determined by how much REAL stuff the country produces (cars, houses, etc) There is no escaping that PHYSICAL FACT.

Turning now to Rajiv Sethi, he quotes Bryan Caplan's post which makes similar arguments about the substitution effect and employer's income and then responds with these arguments:

"Let's take this step by step. First, consider the claim that cutting wages increases the quantity of labor demanded. Through what mechanism does this occur? Consider a firm (McDonald's, say) that can now pay its workers less. It will certainly do so. But will it increase the size of its workforce? Not unless it can sell more burgers and fries. Otherwise its newly expanded workforce will produce a surplus of happy meals that will (unhappily) remain unsold. And this will not only waste the expense of hiring and training new workers, it will also waste significant quantities of meat, potatoes and cooking oil. So the firm will make do with its existing workforce until it sees an uptick in demand. And no cut in the minimum wage will automatically provide such an increase in demand. As a result, the immediate effect of a cut in the minimum wage will be a decline in total labor income."

This of course ignores that a lower cost of labor will likely induce McDonald's to lower its price of happy meals and other items as the semi-fixed cost that labor costs constitute declines, something which given the above mentioned fact that wage negotiations are a zero sum games between employers and employees and will thus not affect demand, will increase demand for labor.

After having assumed that employer's income would not rise in his analysis of the substitution effect, Sethi misleadingly jumps to an analysis of the income effect where the substitution effect is completely ignored.

"Employer income, of course, will rise. Some of this will be spent on consumption, but less than would have been spent if the same income had been received by low wage earners. The net effect here is lower aggregate demand. But wait, what will happen to the remainder of the increase in employer income? It will not be placed under mattresses, on this point I agree with Caplan. It will be used to accumulate assets. If these are bonds, then long rates will decline, and this might induce increases in private investment. Then again, it might not, unless firms believe that additions to productive capacity will be utilized. And right now they do not: private investment is not being held down by high rates of interest on long-term debt.

Finally, what if employers use the unspent portion of their augmented income to buy shares? We would have a run up in stock prices not unlike that we have seen in recent months. Note that this would not be a speculative bubble: the higher prices would be warranted given that firms have lower labor costs. But would this asset price appreciation stimulate private investment in capital goods? Again, not unless the additional capacity is expected to be utilized."

First of all, his assertion that lower long-term interest rates won't affect investment demand is an assertion completely without any empirical or theoretical assertion. He simply asserts it. If long-term rates had been zero, he would have been able to point to the zero bound barrier, but since long-term rates are way above that, this defense won't hold.

And secondly, because the increase in employer's income will come through higher margins, this will induce employers to hire more, and invest more in capital goods.

Moreover, the "wealth effect" of higher stock prices would increase aggregate demand further.

Congratulations to Stefan for tumbling to the crucial and central issue here: the “wealth effect”. Economists in the 1930s tumbled to this one, Pigou in particular. Indeed, the wealth effect stemming from an all-round pay cut is often called the “Pigou effect”. The fact that Stefan does not cite Pigou suggest he has not read the literature. The Pigou effect consists of the following.

Given an all-round pay cut, prices will sooner or later fall by the same amount. That in turn increases the value of money, which in turn makes people feel richer, which in turn induces them to spend more, which in turn raises employment.

Strictly speaking, it is only the monetary base that is relevant here, because in the case of commercial bank created money, every dollar (i.e. asset) is matched by a liability. That is because when a commercial bank extends a loan to person X, the latter spends it on goods made by person Y, Z, etc who deposit the “money” in their banks. The liability of X to X’s bank is matched by the asset (i.e. the money) deposited by Y, Z, etc in their banks.

But as Keynes and others rightly pointed out, the Pigou effect takes far too long to work.

Saturday, September 4, 2010

Kenneth Rogoff.

In an article entitled “Why America Isn’t Working” Kenneth Rogoff displays his ignorance yet again. He gives three reasons for thinking that tax cuts won’t boost the economy.

First, he claims that stimulus involves more debt. Well, as Milton Friedman (and Keynes) explained, one can boost economies WITHOUT extra debt (AND without dropping interest rates). For Milton Friedman’s explanation see http://www.jstor.org/pss/1810624

Second, Rogoff claims that households will save a significant portion of tax cuts, well OF COURSE THEY WILL!!! Households are DELEVERAGING, as everyone, including the average mentally retarded six year old knows by now. When households have been fed enough money via tax cuts and feel comfortable with their levels of leverage, they’ll start spending again. Presumably Rogoff would advocate not pouring water on a house fire on the grounds that the first ten gallons won’t have much effect.

Of course that is not to say simple straightforward stimulus is a panacea. That is, the credit crunch occurred because of risky and fraudulent bank and mortgage practices. That needs rectifying. And the excessive number of former construction industry employees need re-allocating and re-training. But former construction industry employees form only a small portion of the unemployment total in the U.S. (unlike Spain). So construction industry unemployment is not much of an excuse for near record levels of unemployment in the U.S.

Wednesday, September 1, 2010

Subscribe to:

Posts (Atom)