Wednesday, September 29, 2010

Message to the Fed: this is the modern monetary theory (MMT) transmission mechanism.

It seems a number of Fed and ex-Fed people have at last tumbled to the fact that there are serious problems with traditional ideas on money supply transmission mechanisms.

This Fed paper to which Warren Mosler draws attention points to the fact that there has been a 2,173% rise in bank reserves in the last two years, with (contrary to text book predictions) almost no effect. Yes you read that right: 2,173%.

The authors of the Fed paper also say “if the quantity of reserves is relevant for the transmission of monetary policy, a different mechanism must be found.”

And then there is Arnold Kling, who worked for a time as an economist for the Fed. He says “I am having an equally hard time understanding modern monetary theory.”

In view of the above, it might be helpful to set out the MMT transmission mechanism. It is very simple and it’s thus (as I see it).

1. The government-central bank machine net spends in a recession. Assuming government wants the relative sizes of public and private sectors to remain constant, some of the money will be spent on hiring extra public sector workers and/or making sure that tax shortfalls don’t result in public sector workers being sacked. That creates employment.

2. There is a multiplier effect from “1”, that is, part of the above additional payroll costs will be spent, which in turn employs more people.

3. The above additional public sector workers will probably save some of their income. That boosts private sector savings. Those savings will not expand for ever. The point will come where the private sector thinks it has enough by way of savings, at which point it will cease saving and will spend, or try to spend all its income. That employs yet more people.

4. While the above boost for the public sector boosts the private sector INDIRECTLY, it is probably desirable to give the private sector a DIRECT boost as well. That can be done by, for example, reducing payroll taxes or income tax. That boosts employees’ take home pay, which in turn will boost their spending, which employs more people.

Doubtless some of the above private sector increase in take home pay, will be saved. The consequences are exactly the same as with the above public sector employees. That is, savings will rise to the point where no more savings are required, etc, etc.

Sunday, September 26, 2010

Von Mises and whether U.S. unemployment is structural.

One of the main claims made ad nausiam by the Von Mises brigade is that recessions are needed so as to rid the economy of what they call “malinvestments”.

The first flaw in this idea is that in any medium size or largish economy, even in periods of full employment, thousands of firms go bust per week and thousands of new firms start up per week. That is, there is a continuous process of disposing of “malinvestments”. Thus the mere existence of malinvestments does not justify recessions.

Second, every economy is stuffed full of malinvestments in that about 25% of industrial capacity is normally unused.

Third, it is a bit of a mystery as to why the existence of thousands of empty houses going to rack and ruin should stop a country’s workforce being employed in non construction type activities. Moreover, the construction industry has not DISAPPEARED as a result of excess house building: it just halved in size, or thereabouts.

Fourth, if excess demand results from easy credit, this will result in excess investment in a WIDE RANGE of industries, plus it will result in inflation. Now inflation in the U.S. was a percentage point or two above target just before the credit crunch: a negligible problem. In contrast, the REAL problem was the grotesque inflation in house prices and ludicrous mortgages being offered, like the famous NINJA mortgages.

This leads to a more plausible argument which might be the basis for thinking that the economy cannot bounce straight back to where it was pre-crunch. This is that a large excess supply of former construction employees amongst the ranks of the unemployed might mean that it will take time to retrain those people, hence hindering a return to full employment as quickly as we would like. So does the evidence for this phenomenon stack up? The answer is “possibly, but it’s a bit doubtful”.

First, if the latter were a significant problem, one would expect to find significantly more former construction employees amongst the unemployed (relative the size of the construction industry) than former members of other industries. This does not seem to be the case if this Roosevelt Institute study is anything to go by: see charts on page 8 here.

In contrast to the above study, and study done by “Oregon Business Report”, paints a slightly more gloomy picture. On the other hand, according to this study, the expansion in numbers employed in the Oregon construction sector between 2001 and 2009 was identical to the contraction 2007 – 9. Now if the workforce are flexible enough to move INTO construction from a variety of other sectors of the economy, presumably they are flexible enough to move back again (though admittedly the contraction was faster than the expansion).

In contrast to the Oregon study Also this study claims that construction workers have no more difficulty finding alternative work than the national average. Since the latter study covers the naton as a whole rather than just one state, it is presumaly more reliable.

As to strictly theoretical considerations. Suppose the level of unemployment at which inflation becomes excessive is 4%. Suppose the proportion of the workforce employed in construction at its height two years ago was 6%. Suppose numbers employed in construction halve, and that of those becoming unemployed, a half have serious difficulty finding other jobs without retraining. That means the proportion of the workforce who are seriously difficult to place is (6/2)/2 which is 1.5%. That in turn means the overall level of employment at which inflation becomes a problem rises from 4% to (4 + 1.5) = 5.5%.

That is an insignificant rise compared to the actual rise over the last two years. Conclusion: there isn't a huge "structural" problem.

Friday, September 24, 2010

Peter Peterson: economic genius.

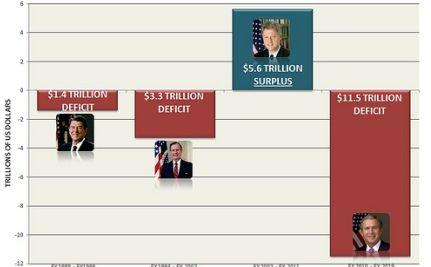

Peter Peterson is a billionaire who spends a significant proportion of his wealth every year promoting the idea that the deficit and national debt must at all costs be reduced. So does he have any particularly bright ideas to back this claim?

The answer is “no”. The ideas put by the Peterson Foundation site are about as simple minded as it is possible to be. The ideas are set out in an article entitled “A Path to Balance”. (There is a link to the article from the Foundation’s site – see the “This paper” link in orange.)

This article is easily comprehensible to a ten year old: that’s how sophisticated it is.

The article starts with two charts, the first of which shows the deficit as a proportion of GDP rising from about zero in 1949 to an average of (shock horror) about 4% for 2001 to 2009. That of course is grossly misleading because in 1949 national debt was at a near record level as a result of WWII and was rapidly being paid back. You’d expect no deficit in those circumstances: indeed you’d expect the occasional surplus. Collecting tax and using the money to pay back the national debt is almost the definition of “surplus”.

Just under that chart is another, showing national debt as a proportion of GDP declining from around 80% in 1949 to roughly 40% in the seventies and eighties, and then rising again to roughly 60% in 2010. What this omits, because it would spoil the Peterson story, is that the debt was over 200% just after WWII. That is, Peterson wants us to think that a rise to much more than the 80% level is some kind of disaster. That’s a bit hard to reconcile with the fact that the debt was well over 200% just after WWII. So we just keep quiet about that, don’t we?

The Peterson master plan is to gradually reduce the debt: a stroke of genius! That sounds much like a household gradually paying off its mortgage. The latter, of course, is microeconomics: about as relevant to paying off a national debt as chalk is relevant to cheese, because national debts, deficits and so on are macroeconomics, whereas individual household mortgages are microeconomics.

The first big problem with gradually paying off national debt at some pre-determined rate over the next ten years or so is that it might be a totally inappropriate policy in say five years time. For example, if there was an outbreak of irrational exuberance and general all round confidence in five years time, with the economy booming and excess inflation just round the corner, then some form of deflationary policy would be needed: for example raising taxes and paying off the national debt much faster than under the above “ten year plan”!

The second big problem is that collecting extra tax (and/or reducing public spending) is deflationary. Thus the basic effect of the “ten year pay back” scheme is deflationary. That could be wholly in appropriate if the economy stays in the doldrums over that period. So what to do?

Well there is an amazingly simple solution. Indeed, this solution could, at least in theory, wipe out the debt in just one year. Here’s how.

First print money and buy the debt back. That on its own would doubtless be too stimulatory and inflationary. Solution: mix the latter policy with a deflationary method of paying the debt back, that is raise taxes (or reduce government spending) and use the money collected/saved to buy the debt back.

Mix the above deflationary and stimulatory/inflationary measures in the right proportion, and you have a neutral pay back arrangement: no excessive inflation or unemployment while paying back. Indeed, the elements of the above solution can be altered to produce any desired outcome. For example for a more stimulatory stance while effecting the pay back, implement a bit more money printing and a bit less tax increase / public spending reduction.

There is just one problem (and one only) with the latter “wipe the national out” system: it would probably involve too much dislocation if started and completed on just one year. That is, it would be difficult to effect without some abrupt changes in the tax paid by particular groups, and that would bring political problems.

But, essentially paying the entire national debt back in a few years, at the same time as adopting any amount of stimulus or deflation you like is not difficult: how to do it can be explained to an intelligent ten year old. For more on this, see here.

Thursday, September 23, 2010

Robert Reich is near to advocating Modern Monetary Theory.

Robert Reich says, quite rightly, that interest rates cannot be dropped any further.

He then points out, correctly, that “The problem is consumers, who are 70 percent of the economy. They can’t and won’t buy enough to turn the economy around.” Agreed.

Put that another way, THE FUNDAMENTAL PURPOSE OF AN ECONOMY is to produce what the consumer wants. In view of this, it might have been an idea, right at the start of the recession, to have given the consumer more of that amazing stuff which ENABLES consumers to go out of buy what they want. And that amazing stuff is called MONEY!!!!!! That would have been better than ar*sing around with interest rates, QE, stuffing the pockets of Wall Street crooks and fraudsters, etc, etc.

Incidentally, in addition to waving their credit cards in the air and demanding various products, consumers also demand (via the ballot box) various publically provided goods and services. So the provision of these also needs to be expanded (or at least not allowed to fall) in a recession – as advocated by Modern Monetary Theory (MMT).

Reich continues: “So what’s the answer? Reorganizing the economy to make sure the vast middle class has a larger share of its benefits. Remaking the basic bargain linking pay to per-capita productivity.” Certainly the middle class (in addition to the lower orders, perhaps) needs more spending power. But there does not need to be a close link between pay and productivity in an MMT scenario.

In particular, come a recession, it would be a good idea to feed more of the above mentioned “amazing stuff” into employees pockets: that is, it is desirable to have employees pay move ahead of productivity, at least for a while. Conversely, given an outburst of irrational exuberance, it would be desirable to have pay fall behind productivity.

Robert Reich: please keep thinking. You’re almost there.

Wednesday, September 22, 2010

Monday, September 20, 2010

Governments taylor their economic policies to account for the economic illiteracy of their populations.

Britain’s finance minister, Alistair Darling, created £60bn out of thin air for the benefit of two banks, RBS and HBOS, when they were in trouble, but didn’t announce what he had done till about eighteen months later. Why? I think it was for much the same reason as Keynes backed a policy he knew quite well was second best.

Keynes said that in a recession governments should borrow and spend. Abba Lerner said governments should just print money and spend it. Keyes was well aware of the “print” option, but seems to have favoured the borrow option because it looked or sounded more respectable or sensible.

Keynes said of Lerner, “"Lerner's argument is impeccable but heaven help anyone who tries to put it across to the plain man at this stage of the evolution of our ideas.”

There is something unhealthy about governments pursuing policies they know to be flawed or second best, simply to take account of the economic illiteracy of the population or the “common man”.

To avoid the above problems in future, the ideal would be to make economics a compulsory school subject, with particular emphasis on when money printing is inflationary and when it is not. But not much chance of that, I suppose.

Thursday, September 16, 2010

I love the ignorance of the anti-stimulus lobby.

“The free market will sort it out….no need for stimulus.” That’s the message of a hundred anti-stimulus articles.

The monster and glaring omission from nearly all these articles is any explanation as to exactly HOW the market gets out of a recession. The latter question was much debated in the 1930s. But, hey you don’t think the anti-stimulus red-necks have actually studied these debates do you?

There ARE actually two mechanisms via which the free market recovers from recessions: the Pigou effect and Say’s law. But Keynes concluded, quite rightly I think, that while these effects work in the long run “in the long run we are all dead”. I.e. these effects do work, but they work too slowly.

But don’t bother trying to find out what the anti-stimulus lobby think about Say or Pigou: most of them haven’t even heard of the two latter indivduals.

Examples of anti-stimulus articles:

1. by Greenspan (of all people):

2. This article is by Garett Jones, a Prof. at George Mason University. In addition to apparently never having heard of Say or Pigou, he seems to think that micro-economic laws work at the macroeconomic level: that is, he thinks that an all round wage cut reduces unemployment. Does he even know there is a distinction between macro and micro?

Subscribe to:

Posts (Atom)