This article by Rogoff is riddled with mistakes. Like Niall Ferguson and Republicans, Rogoff suffers from “debtphobia”. That’s a negative psychological reaction to the overtones and innuendo of the word “debt”: bailiffs knocking at the door, etc. As for any DECENT QUALITY ANALYSIS of debt, that is thin on the ground.

He starts by referring to what he calls “the world’s most pressing macroeconomic problems” – bit of a vague category of problems don’t you think? Anyway, an example of these problems is that “Japan, meanwhile is running a 10%-of-GDP budget deficit, even as growing cohorts of new retirees turn from buying Japanese bonds to selling them.”

The suggestion here is that because a number of “retirees” are selling their government debt, the Japanese government is having problems selling its debt. Well the Japanese government JUST ISN’T having any such problems because they’re paying a negligible rate of interest on the debt. Doh!

What Keynes didn’t say.

Rogoff then goes on to say in relation to these problems (whatever they are): “One extreme is the simplistic Keynesian remedy that assumes that government deficits don’t matter when the economy is in deep recession; indeed, the bigger the better.” Nope.

Keynsians do not think that as regards the debt or deficit, it’s a case of “the bigger the better”. To quote Keynes himself, he said “Look after unemployment and the budget will look after itself”. That is, the deficit needs to be big enough to reduce unemployment as far as is compatible with avoiding too much inflation.

Deficits do not necessarily mean more debt.

Then later in the article (para starting “But who is being naïve?”) Rogoff makes the popular assumption that a deficit necessarily means increased debt.

As Keynes, Milton Friedman, MMTers and others have pointed out, a deficit can perfectly well accumulate as additional monetary base instead of extra debt. Indeed, this is exactly what has happened in several countries over the last two years or so as a result of QE.

To be pedantic, QE does not dispose of debt: it puts the debt into the hands of the central bank. But the central bank is just part of the overall government machine. So that debt might just as well be torn up, as I pointed out in the Financial Times.

Apparently studying Keynes and Friedman is not a requirement when applying for the job of professor of economics at Harvard.

Budgets balance over the cycle?

Rogoff then makes the conventional, but absurd claim that “It is quite right to argue that governments should aim only to balance their budgets over the business cycle…”

If Rogoff actually LOOKED AT the budget figures for his native U.S. or almost any other Western country since WWII, he’d find that budgets just HAVEN’T balanced over the cycle. Put another way, while there is the occasional “surplus year”, most countries run deficits in about nine years out of ten. That is, it’s basically a case of a constant and non-stop deficit. And there is a very simple reason for this, as follows.

Given the 2% inflation target that most countries go for, that inflation necessarily means the national debt and monetary base will shrink at 2% a year in real terms (or at whatever rate of inflation actually occurs). Assuming the national debt and monetary base are going to remain constant relative to real GDP (which roughly speaking is the reality over the decades) that means both have to be topped up in nominal terms on a regular basis. And that means a more or less constant deficit.

In addition, there is the fact that real GDP expands more or less year after year. And that means even more “topping up” if the national debt and monetary base are to remain constant relative to real GDP.

Private Sector Net Financial Assets.

Arguably the above point about 2% inflation leading to a PERMAENT deficit is a bit pedantic. However a more fundamental criticism of the idea that the budget should balance over the cycle is thus.

The private sector, for reasons best known to itself, may decide it wants an increased or reduced stock of what MMTers call “Private Sector Net Financial Assets” (PSNFA): that’s monetary base and government debt. This phenomenon has actually occurred over the last couple of years or so: that is, as is fairly predictable, a reaction to fingers being burned as a result of the crunch has been a desire by the private sector to save, i.e. hoard additional PSNFA.

Now where this desire to hoard arises, the government / central bank machine will just have to supply additional PSNFA, else we get paradox of thrift unemployment.

So, far from it being desirable to “balance the budget over the cycle”, the budget should be whatever supplies the private sector with the PSNFA it wants. And that could for example be be a deficit lasting two cycles, followed by a surplus lasting for another two cycles.

Paying back debt is not deflationary.

Next, he makes the appealing but nonsensical claim that we should be wary of debt financed stimulus because the debt will eventually have to be paid back. And in connection with repaying this debt he says, “The drag on growth is more likely to come from the eventual need for the government to raise taxes…”

The first weakness in that point is that in reality much of the debt gets whittled away in real terms by inflation.

Second, as long as the real or inflation adjusted rate of interest paid on debt is around zero (which it is in the U.S., U.K. and Japan for example), the debt can be left in place ad infinitum if need be: there is no need to repay it and endure any sort of “drag on growth”.

Third, there is of course the possibility (which clearly gives Rogoff and Niall Ferguson nightmares) that the private sector becomes less willing to hold government debt, with the result that interest paid on such debt rises.

Rogoff obviously thinks that the only way debt can be paid back is for government to raise taxes and pay back the debt. And indeed any such “raise taxes and pay back debt” policy would indeed be deflationary.

In fact, a national debt can be paid off with no deflationary (or stimulatory) effect at all. All the relevant government need do is to proceed as follows.

Step No.1: as Rogoff suggests, raise taxes and pay off some debt. That, as Rogoff rightly suggests is deflationary. So enter step No.2 stage left: get some of the money for the debt “pay back” from simply printing new money. The latter has a stimulatory or inflationary effect. And as long as the deflationary effect of the tax increase equals the latter deflationary effect, then the debt is reduced with no overall stimulatory or deflationary effect. QED.

A technicality relating to foreigners.

To be strictly accurate, the above point about paying back debt not being deflationary is 100% true in that the debt is held by domestic entities. In contrast, debt held by FOREIGN entities is different. If (and only if) foreigners withdraw their money from a country on being paid back money in exchange for the debt they hold, there is obviously a foreign exchange hit for the country concerned. But that “hit” will have been balanced by a foreign exchange benefit when foreigners originally bought their debt. So this “foreign” point is a bit of an irrelevance. For more on this see here.

Conclusion:

I rather sympathise with those Harvard economics students for walking out of their lectures (Rogoff and Ferguson are both Harvard academics).

___________

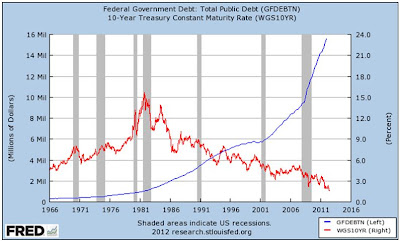

P.S. (13th June 2012). Here is something for the Rogoff / Ferguson doomsday brigade to think about. The idea that an increased debt will lead to an interest rate spike, is – how can I put it – not exactly supported by this chart, which comes to us thanks to Mike Norman. Debt has soared over the last twenty years, while interest rates have plummeted!

Of course this is all a bit misleading, for example the high nominal interest rates around 1980 were to a significant extent compensation for inflation. That is, REAL interest rates were not as high as they would seem from the chart. Plus it is undeniable that if debt rises relative to GDP, all else equal, rates WILL RISE at some point.

But it’s a nice chart all the same.

No comments:

Post a Comment